St. Petersburg Paradox – How To Actually Price Uncertainty?

Published on July 27, 2022 by Hemanth

--

The St. Petersburg paradox represents a key realisation in the history of applied mathematics. It first emerged in the early eighteenth century and engages the finest mathematical and philosophical brains until this very day. “What is so special about it?” you ask?

Well, human beings have to make decisions under uncertain conditions all the time. One of the most prominent mathematical tools we have developed to aid us in this process is the notion of the expected value. If you wish to learn about expected value in detail, check out my essay on the topic.

The St. Petersburg paradox exposed the limitations of expected value theory and paved the foundations of expected utility theory. Furthermore, it made philosophers and psychologists question the nature of human decisions. We benefit from technical discussions on this paradox even today.

In this essay, we will begin by looking at the origins of the St. Petersburg paradox. Following this, we will dive into the mathematics and philosophy behind it. Finally, we will cover how one could solve this paradox and potentially benefit from the solution in real-life applications. Let us begin.

The St. Petersburg paradox gets its name from one of the most prominent scientific journals of the eighteenth century: Commentarii Academiae Scientiarum Imperialis Petropolitanae (Papers of the Imperial Academy of Sciences in Petersburg).

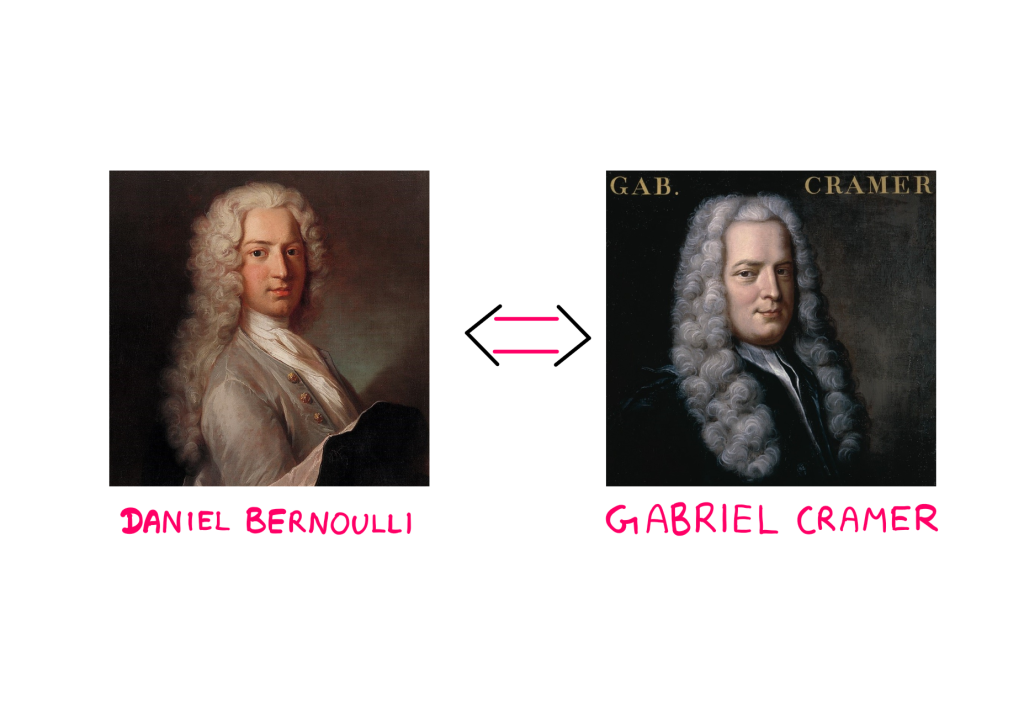

In 1738, Daniel Bernoulli published a paper titled “Specimen Theoriae Novae de Mensura Sortis (Exposition of a New Theory on the Measurement of Risk)”. This paper discussed a seemingly simple probability game that gave a counter-intuitive realisation about pricing unknowns (risk) using the expected value theory.

But Daniel Bernoulli had not invented this game. He had learned about it from his cousin Nicolaus Bernoulli, who had discussed it for the first time in a letter to Pierre Rémond de Montmort in 1713.

N. Bernoulli’s initial version of this game was unnecessarily complicated (using six dice). In this essay, we will look at a simplified version instead.

How Much Should You Pay for this Game?

Let us say that I keep flipping a fair coin until heads comes up for the first time. If heads occurs on the first flip, you get $2. If heads occurs on the second flip, you get $4, and so on.

Essentially, you win $2^n, where n is the total number of times I had flipped the coin to reach the first heads. The question Bernoulli asked was the following:

“How much should you pay to enter this game?”

Surely, you did not think that you would get to play the game for free, did you? There’s a price; there’s always a price. So how shall we go about this?

A Crash Course on Expected Value

If you haven’t read my essay on expected value yet, here is a short crash-course to bring you up to speed: we calculate the expected value of an uncertain bet by multiplying the value of each possible outcome with its probability and summing up all the terms.

According to expected value theory, your decision about the uncertain bet should aim to maximise the expected value. In other words, the higher the expected value, the higher the bet is worth paying for. Now, let us proceed to calculating the expected value of this little problem.

The St. Petersburg Paradox Revealed

A fair coin has a 50% (½) chance of landing heads. If we get heads right on the first flip, you get $2. There is a 25% (¼) probability of getting tails on the first flip and heads on the second flip. In this case, you get $4. If we keep extending this logic further, we arrive at the following summation series:

Expected Value — Math illustrated by the author

So, the expected value of our little game tends to infinity. Does this mean that you should give me everything you own (and more) so that you can play this game? That sounds absurd, right?

Well, based on my gut feeling, I would pay no more than $5 to enter this game. This is the St. Petersburg paradox. It reveals the disconnect between human intuition for expected value and the mathematical notion of expected value.

Note that there is no logical contradiction here; the St. Petersburg paradox belongs to the veridical paradox category. In any case, how shall we solve this disconnect? An acquaintance of N. Bernoulli had an idea.

How to Solve the St. Petersburg Paradox?

Even before D. Bernoulli had published his paper, a Geneva mathematician named Gabriel Cramer had read about N. Bernoulli’s problem in a book published by Montmort. In fact, the simplified version of the St. Petersburg game we are solving in this essay was originally proposed by Cramer.

Cramer’s proposed solution went outside of the realm of conventional mathematics and paved the way for modern applied mathematics and decision theory. He argued that monetary value is subjective and the notion of expected value should not guide the decision on the bet.

Instead, he argued that money starts to saturate in value beyond a certain point. For example, twenty million is not worth ten million more than ten million, because the first ten million would be enough for satisfying all the needs and desires of a rational player.

He came up with two ways of solving the St. Petersburg paradox.

The Upper Bound Solution

Even though the expected value of the St. Petersburg game tends to infinity, we know that worldly monetary resources are finite. So, Cramer proposed an upper bound to the prize money for the game.

If we set 2^m as the upper bound, then the game would end if the coin lands on heads on or after the m-th flip. This way, there are still an infinite number of possibilities but the outcome and the expected value are finite.

This approach has its shortcomings, however, and Cramer was aware of them. Firstly, it is controversial to claim that an upper boundary exists. Any mathematician would argue that just because worldly resources are finite doesn’t mean that the expected value should not be allowed to tend to infinity.

Besides, the problem reappears when we take infinite real-world resources into account. Now, I came up with this thought experiment on my own. But I am pretty sure that some clever soul has already thought of this before. Imagine that we switch dollars with grains of sand as the prize.

If you get heads on the first flip, you get 2 grains of sand, and so on. All of a sudden, an upper bound is not acceptable anymore, and the paradox re-emerges. That’s where Cramer’s second solution comes in handy.

The Moral Value Solution

In this approach, instead of imposing an upper bound, Cramer reduced the speed of growth of monetary value by proposing the following: we could define the moral value of goods as the square root of the corresponding mathematical quantities.

If that is too abstract for you, here is how the improvised summation series would look:

Expected Value — Math illustrated by the author

Cramer used this summation series to compute the value of the bet as roughly $2.9. It turns out that my gut feeling was off by $2.1.

Using such a definition of moral value, the value of additional wealth never reaches zero, but one gains lesser and lesser as he/she increases his/her wealth further. Cramer had implicitly proposed what modern economists would refer to as decreasing marginal utility.

In other words, this was the origin of the expected utility theory.

Conclusion

In his 1738 paper, D. Bernoulli proposed a very similar solution where he defined the utility of wealth as the logarithm of the monetary amount. This way, as one accumulated more wealth, the value of money is saturated as per the logarithmic curve. Bernoulli was aware that Cramer’s solution was conceptually close to his own and gave due credit to him in his paper.

After all these years, the St. Petersburg paradox is a rich source of insight and discovery even today. I would not blame you if you feel that this is an abstract concept with little practical value. But I assure you that there is practical value beneath the layers of abstraction.

I personally attribute a healthy portion of my income in life to the knowledge I have gained from studying this paradox. The current state-of-the-art solution to St. Petersburg paradox is based on something known as the Ergodicity theory.

Since Ergodicity is an advanced concept that deserves its own space, I plan to cover it in more detail in a follow-up essay.

If you’d like to get notified when interesting content gets published here, consider subscribing.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-advertisement

1 year

Set by the GDPR Cookie Consent plugin, this cookie is used to record the user consent for the cookies in the "Advertisement" category .

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

CookieLawInfoConsent

1 year

Records the default button state of the corresponding category & the status of CCPA. It works only in coordination with the primary cookie.

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Cookie

Duration

Description

_gat

1 minute

This cookie is installed by Google Universal Analytics to restrain request rate and thus limit the collection of data on high traffic sites.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Cookie

Duration

Description

__gads

1 year 24 days

The __gads cookie, set by Google, is stored under DoubleClick domain and tracks the number of times users see an advert, measures the success of the campaign and calculates its revenue. This cookie can only be read from the domain they are set on and will not track any data while browsing through other sites.

_ga

2 years

The _ga cookie, installed by Google Analytics, calculates visitor, session and campaign data and also keeps track of site usage for the site's analytics report. The cookie stores information anonymously and assigns a randomly generated number to recognize unique visitors.

_ga_R5WSNS3HKS

2 years

This cookie is installed by Google Analytics.

_gat_gtag_UA_131795354_1

1 minute

Set by Google to distinguish users.

_gid

1 day

Installed by Google Analytics, _gid cookie stores information on how visitors use a website, while also creating an analytics report of the website's performance. Some of the data that are collected include the number of visitors, their source, and the pages they visit anonymously.

CONSENT

2 years

YouTube sets this cookie via embedded youtube-videos and registers anonymous statistical data.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

Cookie

Duration

Description

IDE

1 year 24 days

Google DoubleClick IDE cookies are used to store information about how the user uses the website to present them with relevant ads and according to the user profile.

test_cookie

15 minutes

The test_cookie is set by doubleclick.net and is used to determine if the user's browser supports cookies.

VISITOR_INFO1_LIVE

5 months 27 days

A cookie set by YouTube to measure bandwidth that determines whether the user gets the new or old player interface.

YSC

session

YSC cookie is set by Youtube and is used to track the views of embedded videos on Youtube pages.

yt-remote-connected-devices

never

YouTube sets this cookie to store the video preferences of the user using embedded YouTube video.

yt-remote-device-id

never

YouTube sets this cookie to store the video preferences of the user using embedded YouTube video.

![St. Petersburg Paradox — How To Actually Price Uncertainty? — Expected value = [(1/2)*2] + [(1/4)*4] + [(1/8)*8] + … = 1 + 1 + 1 + … = Tends to infinity](https://miro.medium.com/max/770/1*2t6E2BqglHFVfb74YVXxhw.png)

![St. Petersburg Paradox — How To Actually Price Uncertainty? — Expected value = [(1/2)*√1 ] + [(1/4)*√2] + [(1/8)*√4] + …](https://miro.medium.com/max/770/1*JL-f2ROW86HC0EVjR15y8g.png)

Comments