Variance: The Reason Why Rich Get Richer And Poor Get Poorer

Published on July 30, 2022 by Hemanth

--

Variance is not the first word that comes to mind when you think about why the rich get richer and the poor get poorer. But in this essay, we will not only see why this is the case, but also find out what expected utility theory has to say about this phenomenon as well.

We will start by pondering upon a hypothetical betting game. Following this, we will see what expected value theory has to say about this hypothetical bet. Next, we will cover what expected utility theory has to say and how variance slots into all of this.

By the end of this essay, you would be able to appreciate some of the mathematics and psychological implications behind financial decisions and financial gains/losses from stock markets, retirement funds, indices, options, etc.

Let us say that you are presented with a fair bet (50% chance of winning) — something like a fair coin toss. If you win, you get two million dollars. If you lose, you lose one million dollars. A simple Game, right?

Would you play this game? That decision is not necessarily simple. We will eventually see why. But first, let us see what expected value theory has to say about this betting game.

The Rational Expectation

If you wish to understand the concept of expected value properly, check out my essay on this topic. But if you are short on time, here is a short crash course to bring you up to speed: we calculate the expected value of a bet by multiplying the value of each possible outcome with its probability and summing up all the terms.

In our case, we have just two possibilities: win or loss (each with a 50% chance of occurring). Consequently, we could calculate the expected value of the bet as follows:

This is what we would call a bet with a positive expected value. In other words, this is a favourable bet. According to expected value theory, you should take it.

But would you? If you feel uneasy about the decision to take the bet, you are not alone. To understand why this bet is not for everyone, let us start looking at things from a different perspective.

The Not So Rational Expectation

You see, a fictitious rational person from a poorly-written economics textbook would take the bet based on expected value. But alas, we are all real people with real-world problems.

Let us say that you are a typical person with measly savings. If you win the bet, you would happily take the two million, not having to worry about working for the rest of your life. But if you lose the bet, you lose more than what you own; you get wiped out!

Consider a multi-national corporation on the other hand. This is not a real person with real-person problems. For such an organization, the expected value bet makes sense. Because losing a million now and then would not hurt the corporation much. But if the corporation takes the bet often enough, it will make $500,000 per bet, on average.

In other words, the law of large numbers has to come into effect for one to benefit from the positive expectation of the bet. Let us say that a loss for the organization equals -1 Utils (a Util is an arbitrary unit of utility). On the other hand, let a gain for the organization equal +2 Utils. So, all in all, the expected utility for the corporation plays out as follows:

It is clear to see that for the organisation, 1 util equals 1 million dollars.

However, for you, winning the bet would be a life-changing gain — let us say you gain +10 Utils. On the other hand, if you lose the bet, you are completely wiped out — let us say you lose -1000 Utils. The expected utility for you looks like this:

Expected utility for you = [50% * (-1000 Utils)] + [50% * (+10 Utils)] = -495 Utils

If we rate your risk on the corporation’s utility scale, your expected utility is -$495 million. It is then no wonder why this bet does not make sense for the typical person. But wait, there’s more!

Picking Up Pennies in Front of a Steamroller

You see, a negative utility value tells us something very significant: not only is taking the bet worse for you than losing $500,000 (the expected value), but it is worse than doing nothing at all!

This is because the bet has an asymmetric outcome for you. You have a 50% chance of winning good money. But at the same time, you run a 50% chance of a complete wipe-out if you take the bet. This is known as “picking up pennies in front of a steamroller” in the biz.You make some money until you eventually get run over.

But this is not the case for the corporation. It would not go bankrupt after a few losses on the bet now and then. So, the positive expected value ensures that the corporation would make money in the long run, on average.

In other words, the richer you are, the more risks you can take with financial bets — as long as the bets have a positive expected value, on average. “Why is this?” you ask? Because the more bank you have, the less you react to variance. Ah, yes! We arrive finally at variance. What does that word mean? Let us find out.

Why Do You Need to Bother with Variance?

So far, we have established that when you take a bet with a significant chance of a wipe-out, you pick up pennies in front of a steam-roller. How can you solve this problem? How about leveraging yourself ten-thousand-folds and taking the same bet? This way, you are up twenty billion if you win and are down ten billion if you lose.

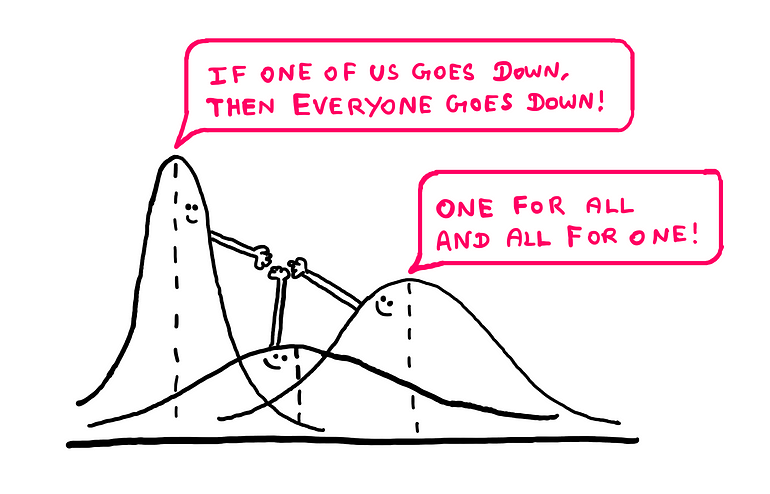

Variance relationships — Illustrative art created by the author

That sound absurd, right? Except, it is not! Our economy is held by weak-forces that act in tandem. If you stand to lose 2 million, it is your problem. But if you stand to lose ten billion, it is the government’s problem! This has historically worked out quite well for many corporations; governments have recently been printing money to keep the markets from going down.

Back to variance — it measures how extreme the possible outcomes of your decision are and how likely you are to encounter these extreme outcomes. When we compare bets with same/similar positive expected value, people generally tend to choose bets with lesser variance.

This is what strategies like portfolio diversification tend to do. When you invest in a big index fund, you are putting your eggs into many baskets. This way, if one basket goes down, the rest do not necessarily go down with it. In other words, lesser variance.

On the other hand, big corporations can tolerate higher variance and stand to gain more in a shorter duration of time. In the case of an impending systemic collapse, the government is likely to intervene (yay!).

Managing Variance and Bank Runs

Mark* is an upcoming hedge-fund manager. Since the last year, he has been developing “sophisticated” financial models and has been seeing good returns. At some point, interested “investors” wanted to give him their money. But Mark* said no to them.

Why? Because, variance! It is true that Mark was seeing good returns. But his models were also running on high variance. Mark knew what he could tolerate in terms of portfolio swings. But he has no way of knowing what external investors can or cannot tolerate.

Most money-management ventures involve tackling variance. When the markets take a nose-dive, people get scared and typically attempt to salvage what they can by withdrawing money from funds. Imagine getting punched in your gut by your best friend when you come to him with stomach ache.

This is called a bank-run or a fund-run. If the fund is not structured properly, it would collapse. This is why most hedge-funds have “lock-in” structures. Investors typically have an enforced waiting period before they can withdraw money. This way, the fund manager can deal with variance without trusting her investors’ psychological stability.

Now, it is time to answer our main question.

Why Do the Rich Get Richer and Poor Get Poorer?

Let us consider two persons: a rich person and a poor person. Both would like to invest in the stock market. If you didn’t know already, the stock market has long-term positive expected value (if we are excluding possibilities of human extinction, annihilation, etc).

Let us say that both persons invest money in the stock market. Although it has positive expected value, the stock market also has considerable variance. When the stock market takes a nose dive (which happens now and then), the poor person’s entire net worth is at risk. She feels the need to save what little she has left from going down further.

The rich person, on the other hand, can take a nose-dive or two now and then without issues. She does not sell during nose-dives, and comes out on top with a positive expected value in the long run, on average.

Variance with Negative Expected Values

When it comes to negative expected values, human psychological behaviour inverses itself. In this case, people prefer a huge variance as opposed to a lesser variance. Let us say that someone is choosing between a sure loss of $3 million and a bet with a 95% chance of a loss of $3 million and a 5% chance of winning $50. The typical person is likely to go for the bet instead of the sure loss.

A sure loss has zero variance, whereas the bet offers a small, yet possible chance of winning with significantly more variance. This explains kamikaze financial decisions and behavioural patterns exhibited by the YOLO (you only live once) wallstreetbets crowd (on reddit).

Summary — What is the Role of Variation in All of This?

Here is a list of everything we just covered in this essay:

1. The expected value model does not take subjective experiences into account.

2. The expected utility model does so — people have different expected utilities for the same amount of money. The relationships are also practically non-linear and dynamic.

3. Poor people are likely to be affected by and buckle under variance.

4. Rich people are likely to be less affected by variance.

5. When big losses involve systemic risks, governments intervene; big corporations take advantage of this.

6. With positive expected values, people tend to minimize variance.

7. With negative expected values, people tend to maximize variance.

So, how can we benefit from all of this information? I would say that we could aim to understand ourselves a little bit better and make more reasonable decisions in life. It helps to be aware of variance.

I know that this is not a one-shot-fix for all financial problems. But if it were that easy, everyone would be rich!

*Mark is a fictional character. Any resemblences with real-life events are purely coincidental.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-advertisement

1 year

Set by the GDPR Cookie Consent plugin, this cookie is used to record the user consent for the cookies in the "Advertisement" category .

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

CookieLawInfoConsent

1 year

Records the default button state of the corresponding category & the status of CCPA. It works only in coordination with the primary cookie.

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Cookie

Duration

Description

_gat

1 minute

This cookie is installed by Google Universal Analytics to restrain request rate and thus limit the collection of data on high traffic sites.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Cookie

Duration

Description

__gads

1 year 24 days

The __gads cookie, set by Google, is stored under DoubleClick domain and tracks the number of times users see an advert, measures the success of the campaign and calculates its revenue. This cookie can only be read from the domain they are set on and will not track any data while browsing through other sites.

_ga

2 years

The _ga cookie, installed by Google Analytics, calculates visitor, session and campaign data and also keeps track of site usage for the site's analytics report. The cookie stores information anonymously and assigns a randomly generated number to recognize unique visitors.

_ga_R5WSNS3HKS

2 years

This cookie is installed by Google Analytics.

_gat_gtag_UA_131795354_1

1 minute

Set by Google to distinguish users.

_gid

1 day

Installed by Google Analytics, _gid cookie stores information on how visitors use a website, while also creating an analytics report of the website's performance. Some of the data that are collected include the number of visitors, their source, and the pages they visit anonymously.

CONSENT

2 years

YouTube sets this cookie via embedded youtube-videos and registers anonymous statistical data.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

Cookie

Duration

Description

IDE

1 year 24 days

Google DoubleClick IDE cookies are used to store information about how the user uses the website to present them with relevant ads and according to the user profile.

test_cookie

15 minutes

The test_cookie is set by doubleclick.net and is used to determine if the user's browser supports cookies.

VISITOR_INFO1_LIVE

5 months 27 days

A cookie set by YouTube to measure bandwidth that determines whether the user gets the new or old player interface.

YSC

session

YSC cookie is set by Youtube and is used to track the views of embedded videos on Youtube pages.

yt-remote-connected-devices

never

YouTube sets this cookie to store the video preferences of the user using embedded YouTube video.

yt-remote-device-id

never

YouTube sets this cookie to store the video preferences of the user using embedded YouTube video.

Comments