When it comes to transactions of value, fiat money is the norm in today’s world. But it was not always like this. In fact, humanity’s collective transition to fiat money happened relatively recently.

Why was fiat money not the norm in the past? And why is it the norm today? To begin answering these questions, one needs to understand how fiat money works, and how it historically came to be.

In this essay, I will try to construct a story-based beginner’s framework for the notion of fiat money. But before I proceed, let me quote Investopedia’s definition of fiat money:

“Fiat money is a government-issued currency that is not backed by a commodity such as gold.”

— Investopedia

If that is all there is to fiat money, why should I bother writing an essay about it? Well, as often is the case with abstract concepts, the simplicity of fiat money turns out to be surprisingly deceptive. In short, there is more than what meets the eye here.

We will eventually uncover what is hiding underneath. But for now, let us begin with a fundamental underlying concept.

When two or more parties exchange goods or services, we call the act “barter”. The notion of barter existed long before the notion of money. I would even argue that barteremerges naturally in other animal species that live in social groups as well.

Let us say that there existed a caveman ‘A’ who gathered berries and wanted some meat. It just happened to be that he lived not far away from a cavewoman ‘B’ who was a hunter. And guess what? She loved berries.

In this scenario, it turned out to be a straightforward barter: A and B agreed on a specific quantity of meat in exchange for a specific quantity of berries. This is how things went on for a long time.

However, as all good things eventually come to an end, so did this relationship between A and B. One day, B decided that she was not into berries anymore.

The Downside of Barter

“I am not into berries anymore. I would like to try some cheese.”, said B to A. The caveman was devastated to hear this. How he wished that cheese grew on plants, but berries were all he had to offer unfortunately.

Luckily for B, there lived a cavewoman named ‘C’ nearby who raised a bunch of goats and had goat-cheese to offer. But at the same time, B being the kind person she was, did not want A to go out of business.

So, she asked C if she was interested in berries. When C revealed that she would like to barter cheese in exchange for berries, B structured the deal such that C got berries from A and A got cheese from C. Then, A gave the cheese to B and B gave her meat to A.

If you feel that this deal-structure is confusing, I am with you. This is indeed unnecessarily complicated and inefficient. Furthermore, what if C did not want any berries? We would have a big problem on our hands. If only there existed a more neutral store of value that all parties could use to trade goods with each other.

The Notion of Token Money

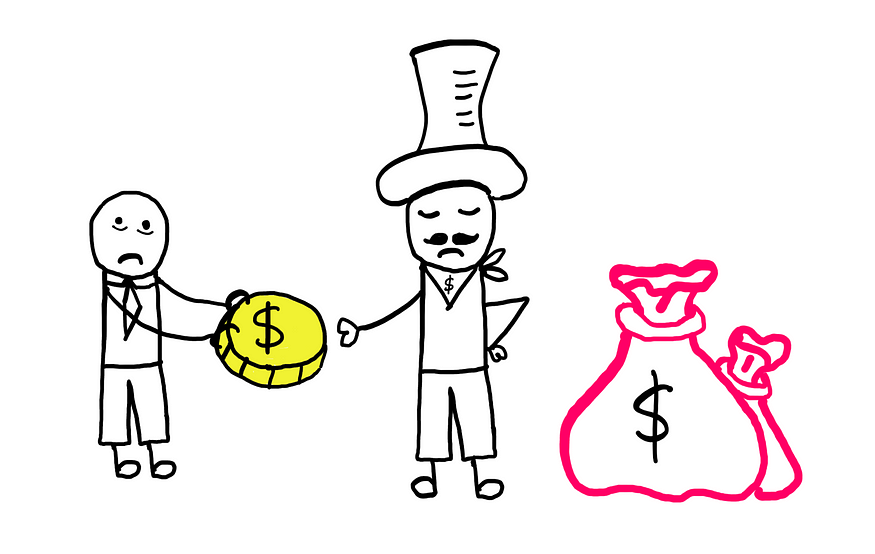

We now fast-forward to the fictional kingdom of Goldland, where the townsfolk solved this problem rather efficiently. As you might have guessed, these folks used gold coins to buy and sell goods.

This was significantly more efficient. There was one problem, however. The richest man in town wanted to buy a huge property. In order to pay for the property, he would need 1000 crates of gold coins. This would have been very expensive to organize.

To mitigate the effort-cost, he gave the seller 1000 custom-made bronze coins with his signature imprinted on them. He told the seller that each of these coins would amount to 1 crate of gold coins that the seller could collect at any time at the rich man’s castle.

Transaction using token money — Illustrative art created by the author

I would like to pause the story here to explain something interesting. The notion of buying and selling using gold coins is known as commodity money. It is a form of token money. Another form of token money is representative money, where the token represents a certain quantity of some commodity (like how each bronze coin represents 1 crate of gold coins).

As we have travelled the time of cave folk to townsfolk, we have seen the efficiency of monetary transactions (and trade) increase from plain barter to transactions involving representative money. But can transactions get even more efficient? Let us continue the story to find out.

The Birth of Fiat Money

A few days after the richest man in town completed this unique transaction, King Goldard-IV came to know of this. With the counsel of his advisor, he wanted to improve the system even more. The wise counsellor came up with the following idea:

“Sire, what if we replaced coins altogether with small slices of printed wood to facilitate financial transactions?”

To this, King Goldard-IV replied:

“That is an excellent suggestion, counsellor. But how can we ensure that each slice of printed wood has value? Our folk may choose to not use the printed slices of wood for their transactions, after all.”

The clever counsellor took his time to think deeply about his King’s worry. After what felt like an eternity, he responded:

“That is easy, my Sire! The slices of wood shall not have any intrinsic value themselves. But as the King, you may hang any folk in our country who does not use these slices for trade.”

And thus, fiat money was born!*

How Does Fiat Money Work?

The word “fiat” comes from Latin, and translates roughly to “let it be done”, in the context of an order or decree from an authority such as a King or a government.

Fast forward to the present, fiat money is slowly transitioning from thin slices of wood to binary digits stored in solid state drives and processed by computers. But the underlying principle has not changed.

How does fiat money work — Illustrative art created by the author

In the developed world, money (be it paper or digits) theoretically does not have any (intrinsic) value by itself. Its value is agreed upon by buyers and sellers in the market. In complex market systems, this value emerges naturally from market equilibrium — the market of buyers and sellers functions like an organism.

In case the market equilibrium breaks, the government or a similar authority (like the central bank) steps in and tries to stabilize the market artificially. These strategies and their consequences can be surprisingly very complex.

I would be happy to dive into the more complex topics (including the questions I posed in the introduction) in a later essay. But for now, I hope you found this beginner’s introduction to fiat money worthwhile. Thank you for reading!

*Update Post Publishing:

My intention here is not to convey that the use of fiat money is enforced by fear, but to point out that there is an enforcing function.

If you think about it, trust and fear are two sides of the same coin. If I give you a few notes in exchange for goods today, how will you know for certain that these notes will be accepted by someone else?

That is where trust in a central authority comes in. Sure, you trust me and others around you to do financial transactions with notes. However, your trust increases by the fact that there is an authority who will enforce the use of notes, should anyone choose to back out.

Once again, thanks for reading!

If you’d like to get notified when interesting content gets published here, consider subscribing.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-advertisement

1 year

Set by the GDPR Cookie Consent plugin, this cookie is used to record the user consent for the cookies in the "Advertisement" category .

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

CookieLawInfoConsent

1 year

Records the default button state of the corresponding category & the status of CCPA. It works only in coordination with the primary cookie.

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Cookie

Duration

Description

_gat

1 minute

This cookie is installed by Google Universal Analytics to restrain request rate and thus limit the collection of data on high traffic sites.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Cookie

Duration

Description

__gads

1 year 24 days

The __gads cookie, set by Google, is stored under DoubleClick domain and tracks the number of times users see an advert, measures the success of the campaign and calculates its revenue. This cookie can only be read from the domain they are set on and will not track any data while browsing through other sites.

_ga

2 years

The _ga cookie, installed by Google Analytics, calculates visitor, session and campaign data and also keeps track of site usage for the site's analytics report. The cookie stores information anonymously and assigns a randomly generated number to recognize unique visitors.

_ga_R5WSNS3HKS

2 years

This cookie is installed by Google Analytics.

_gat_gtag_UA_131795354_1

1 minute

Set by Google to distinguish users.

_gid

1 day

Installed by Google Analytics, _gid cookie stores information on how visitors use a website, while also creating an analytics report of the website's performance. Some of the data that are collected include the number of visitors, their source, and the pages they visit anonymously.

CONSENT

2 years

YouTube sets this cookie via embedded youtube-videos and registers anonymous statistical data.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

Cookie

Duration

Description

IDE

1 year 24 days

Google DoubleClick IDE cookies are used to store information about how the user uses the website to present them with relevant ads and according to the user profile.

test_cookie

15 minutes

The test_cookie is set by doubleclick.net and is used to determine if the user's browser supports cookies.

VISITOR_INFO1_LIVE

5 months 27 days

A cookie set by YouTube to measure bandwidth that determines whether the user gets the new or old player interface.

YSC

session

YSC cookie is set by Youtube and is used to track the views of embedded videos on Youtube pages.

yt-remote-connected-devices

never

YouTube sets this cookie to store the video preferences of the user using embedded YouTube video.

yt-remote-device-id

never

YouTube sets this cookie to store the video preferences of the user using embedded YouTube video.

Comments