The rule of 72 is a quick back-of-the-envelope investment calculation technique. Non-technical investors use the rule to estimate how long it would take to double an investment given a fixed rate of return. The rule of 72 has gained popularity among mainstream investors over the years primarily due to its simplicity.

For anyone just interested in the final result, it is an easy way to arrive at rough estimations. This way, they need not get involved in the mathematics behind the rule. However, there are certain costs involved in simplified mathematics that we cannot overlook.

In this article, I will dive into the mathematics behind this rule, and explore its limits in terms of the accuracy of results and assumptions involved.

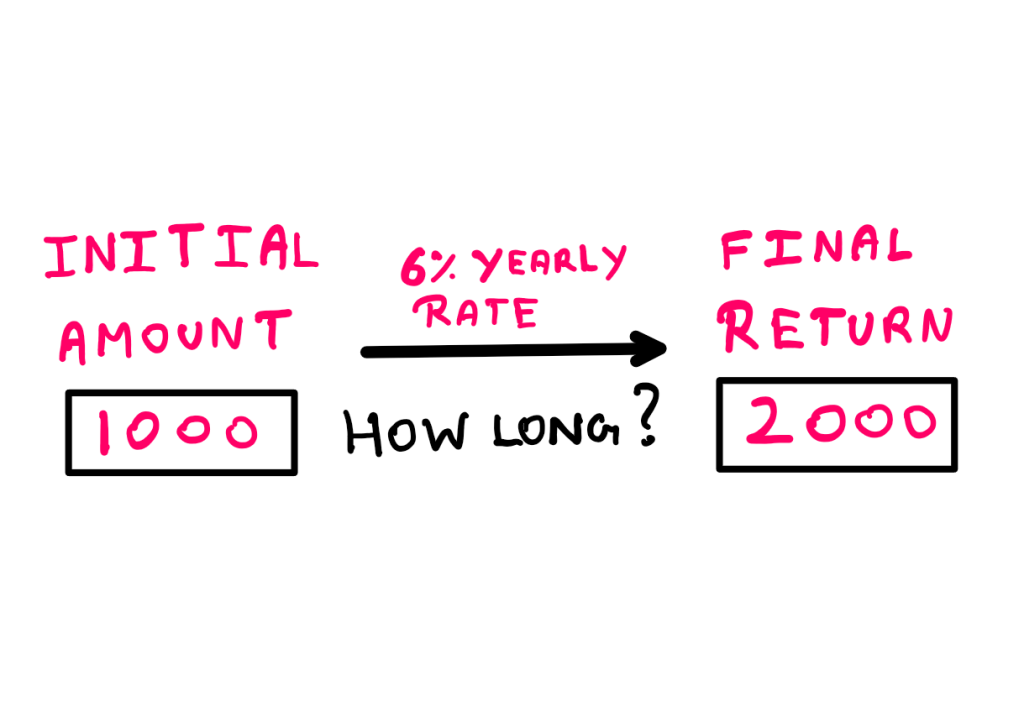

Let us say that you are the typical non-technical investor. You have discovered an investment opportunity that gives you a fixed yearly compounded rate of return, say, 6%. You have an investment capital of 1000 monetary units at your disposal. You are now interested in (mentally) estimating how long it would take for this capital to double if you chose to invest.

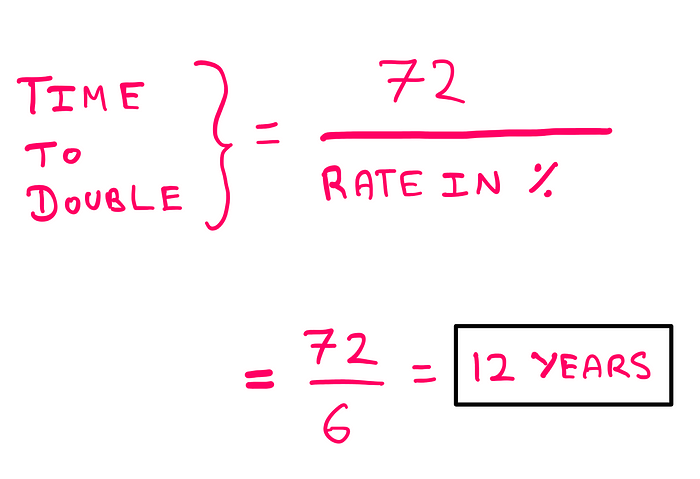

You can take advantage of the rule of 72 by simply dividing 72 by the rate of return (in percentage). This would give you the time (in years in this case) it would take for your capital to double.

Math illustrated by the author

So, as an investor who is just interested in the final result, you get a quick estimate that it would take your initial capital about 6 years to double. Based on this back-of-the-envelope calculation, you may choose to invest or pass.

Now that we’ve seen how the rule of 72 works, it is time to get into the mathematics behind it. But before that, let us spend some time on the implicit assumptions the rule makes.

The Assumptions Behind the Rule of 72

The rule of 72 cannot just be applied to any investment. The first implicit requirement for the rule is that it can only be applied to investments that compound at a constant rate over time.

Will Kenton states another not so obvious implicit assumption from the rule of 72 as follows:

“The Rule of 72 applies to compounded interest rates and is reasonably accurate for interest rates that fall in the range of 6% and 10%.”

Why is this the case? To understand the implicit assumptions behind the rule of 72, we will have to get into the mathematics behind the rule.

The Mathematics Behind the Rule of 72

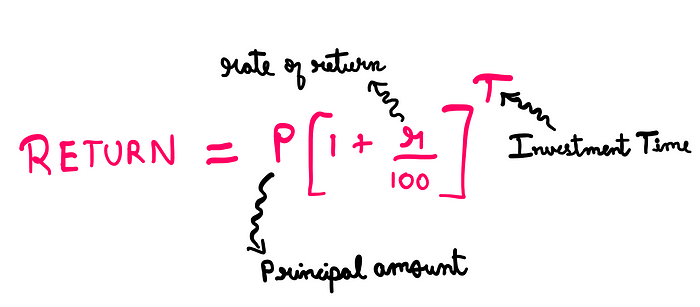

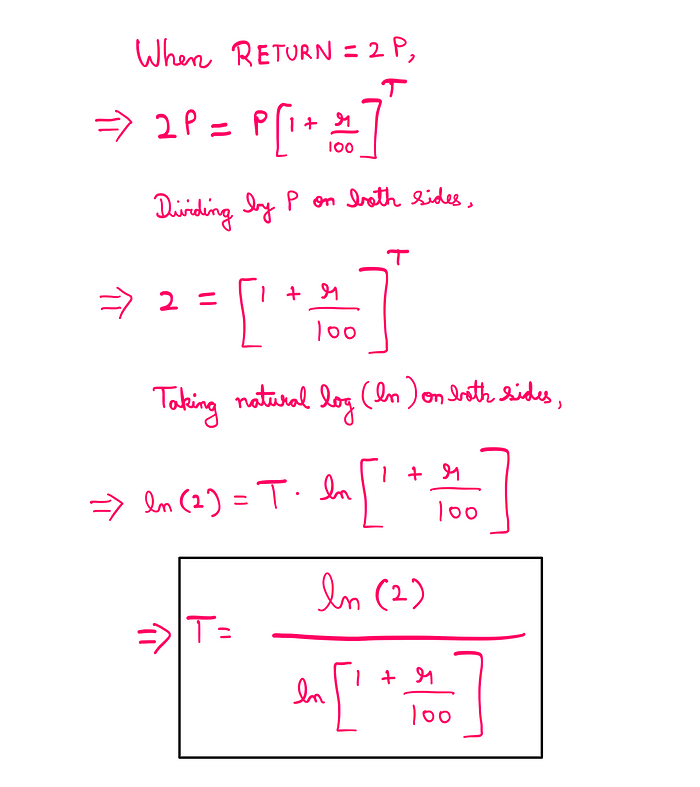

The formula for any investment return from a given principal amount (P) and a fixed rate of return (r) per compounding frequency over a total investment time (T) is defined as follows:

Math illustrated by the author

Now, let us say that we require the return be equal to 2P (double the principal amount). This would enable us to calculate the time taken (T) to double the initial investment as follows:

Math illustrated by the author

This gives us the precise formula to calculate the time taken to double any principal amount given a compounded rate of return.

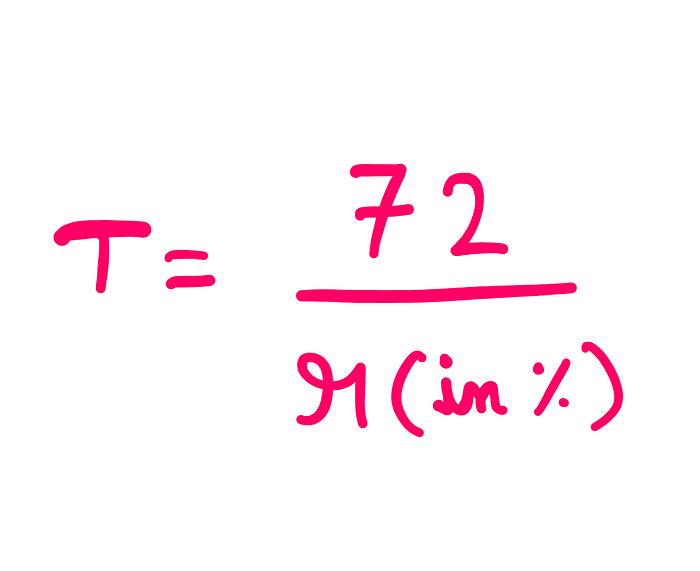

The rule of 72 is a rough simplification of the above formula for people who are not interested in multiplicative dynamics or logarithms. It supposedly takes advantage of the following two facts:

1. ln(2) is approximately equal to 72%

2. ln(1+(r/100)) is approximately equal to r when the value of r ranges between 6% and 10%.

Applying these two approximations, non-technical investors transform the original formula as follows:

Math illustrated by the author

If you are the mathematical type, and your scepticism-meter is twitching, you are in good company. This does look like a recipe for poor results. So, let us proceed to investigate this approximation further.

Technical Investigation into the Rule of 72

Let us now directly challenge the two major mathematical approximations of the rule of 72 that we just covered.

From the first point, we see that ln(2) is much closer to 69% than 72%. The rule should have ideally been named ‘the rule of 69’. But why has it turned out to be the rule of 72?

It could be because of the fact that 72 has many more factors than 69. Hence, for the typical non-technical investor, it is probably easier to divide 72 by the various interest rates as compared to dividing 69.

From the second point, we see that there are potentially significant deviations in the interest rate consideration as well.

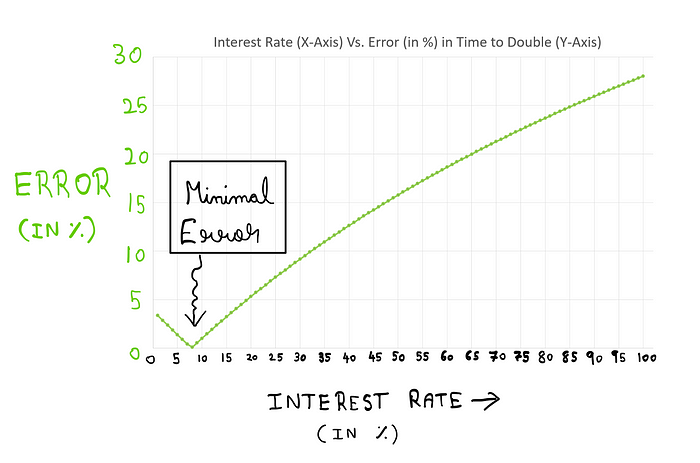

Combining these two factors, if we plot the error in investment-doubling-time approximation from the rule of 72 versus the accurate result from the actual formula (involving natural logarithms), we get the following result:

Interest Rate Vs. Error Plot — created by the author

The error is the least (ranging between 0% and 1%) when we use the rule of 72 for interest rates ranging between 6% and 10%. So, it becomes quite clear why Investopedia suggests this as the acceptable range of applicability for the rule of 72.

From the error chart, we can safely say that the higher the interest rate on the right side of 10%, the higher the calculation error would be.

Having investigated the mathematics behind the rule of 72, there are a few more points that one needs consider to ensure its responsible usage.

Responsible Application of the rule of 72

One of the primary issues with the application of the rule of 72 is the fact that most people using the rule are ill-aware of its implicit assumptions. The rule is often distributed via word-of-mouth or its social media equivalents. One does indeed come across as a clever investor when one is able to spit out quick estimates.

However, beyond the suggested (interest rate) percentage range, the application of this rule becomes very questionable. I’ve come across approaches where ‘experts’ suggest transforming the rule into ‘the rule of 73/74/75/…’ based on the interest rate being used.

These approaches revolve around the idea of minimizing the error by manipulating the numerator in the direction of the original formula’s result. In short, we arrive at a chart featuring different numerators that are applicable over different ranges of interest rates.

At this point, the calculation process becomes so cumbersome that the whole allure of the ‘rule of 72’ breaks down. I would suggest that you drop the rule altogether and just use the original formula (wherever applicable). In fact, if you could just get into terms with the idea of using natural logarithms, the original formula is not that complex at all.

Final Thoughts

Asa final thought, it is important to point out that the rule of 72 is meant to be applied to investments with a constant compounding rate. In the case of most real-world investments, a constant compounding rate is simply not available or possible. This naturally disqualifies the rule of 72 for most real-world investments.

It is at best just good enough for quick hypothetical estimates, but not much more. I have come across cases where people compute arithmetic averages of return rates over time and then use the rule of 72 to forecast doubling time.

I would also recommend against such practices. The average of a function is unfortunately not always equal to the function of the average. This leads to a bigger can of technical worms which is perhaps a topic for a future article. But for now, the knowledge that the rule of 72 applies only to constant rates of return should suffice.

In the end, when using any ‘rule’ that has a mathematical basis, the user should ideally understand the mathematics behind the so-called rule. As tedious as this may sound, it is the only way to ensure responsible application of such a rule, and thereby, ensure optimal results!

I hope you found this article interesting and useful. If you’d like to get notified when interesting content gets published here, consider subscribing.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-advertisement

1 year

Set by the GDPR Cookie Consent plugin, this cookie is used to record the user consent for the cookies in the "Advertisement" category .

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

CookieLawInfoConsent

1 year

Records the default button state of the corresponding category & the status of CCPA. It works only in coordination with the primary cookie.

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Cookie

Duration

Description

_gat

1 minute

This cookie is installed by Google Universal Analytics to restrain request rate and thus limit the collection of data on high traffic sites.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Cookie

Duration

Description

__gads

1 year 24 days

The __gads cookie, set by Google, is stored under DoubleClick domain and tracks the number of times users see an advert, measures the success of the campaign and calculates its revenue. This cookie can only be read from the domain they are set on and will not track any data while browsing through other sites.

_ga

2 years

The _ga cookie, installed by Google Analytics, calculates visitor, session and campaign data and also keeps track of site usage for the site's analytics report. The cookie stores information anonymously and assigns a randomly generated number to recognize unique visitors.

_ga_R5WSNS3HKS

2 years

This cookie is installed by Google Analytics.

_gat_gtag_UA_131795354_1

1 minute

Set by Google to distinguish users.

_gid

1 day

Installed by Google Analytics, _gid cookie stores information on how visitors use a website, while also creating an analytics report of the website's performance. Some of the data that are collected include the number of visitors, their source, and the pages they visit anonymously.

CONSENT

2 years

YouTube sets this cookie via embedded youtube-videos and registers anonymous statistical data.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

Cookie

Duration

Description

IDE

1 year 24 days

Google DoubleClick IDE cookies are used to store information about how the user uses the website to present them with relevant ads and according to the user profile.

test_cookie

15 minutes

The test_cookie is set by doubleclick.net and is used to determine if the user's browser supports cookies.

VISITOR_INFO1_LIVE

5 months 27 days

A cookie set by YouTube to measure bandwidth that determines whether the user gets the new or old player interface.

YSC

session

YSC cookie is set by Youtube and is used to track the views of embedded videos on Youtube pages.

yt-remote-connected-devices

never

YouTube sets this cookie to store the video preferences of the user using embedded YouTube video.

yt-remote-device-id

never

YouTube sets this cookie to store the video preferences of the user using embedded YouTube video.

Comments